Topics

Topics

Cracking Down on Pass-Throughs

In 2016, a consortium of journalists exposed how a global elite including associates of Russian President Vladimir Putin, the King of Saudi Arabia, drug dealers, and others hid their wealth (legally and illegally) using a network of shell companies and offshore tax havens. Known as the “Panama Papers” investigation, their project revealed how the wealthy and powerful use shell companies to hide billions in wealth and income from taxation, among other crimes. But when the papers were released, some questioned why there were so few Americans named. The answer, per one expert, was that Americans “really don’t need to go to Panama. Basically, we have an onshore haven industry in the U.S. that is as secretive as anywhere.” Like their global counterparts, elite Americans increasingly use untaxed pass-through businesses to avoid taxes and pass money overseas, driving inequality ever higher.

![]()

The secrecy, flexibility, and tax advantages of pass-through businesses have made them the preferred income source for the wealthy. Unlike traditional C-corporations (think Alphabet, General Motors), which pay corporate taxes and dividend taxes on their profits, pass-through businesses (think private equity firms and real estate firms) pay no federal taxes on their regular profits. Instead, profits flow onto owners’ personal returns. In theory, those profits are then taxed at personal income rates. In practice, taxes on pass-through income are low, especially after the 2017 Tax Cuts and Jobs Act cut the top tax rate on most partnership income to 29.6 percent versus 37 percent for regular income.

The numbers bear out how pass-through businesses drive inequality. The Congressional Budget Office (CBO) reports that since 1980, the top 1 percent of individual earners have seen their incomes grow by 324 percent after inflation, compared to just 45 percent for the middle quintile. The fastest-growing slice of that income is pass-through business income, which has surged more than 1,000 percent since 1980. One study found that 41 percent of the increase in inequality from 1980 to 2013 was due to the rising use of pass-through businesses by the top 1 percent of Americans.

To make matters even worse, the pass-through business sector is now one of the easiest places for the rich and powerful to evade or avoid taxes using shell companies. Pass-through businesses and their accountants have largely triumphed in their long-running battle to make it impossible for the IRS to audit and track their operations. Since pass-through businesses pay no federal taxes, there is no penalty for creating dozens or hundreds of such entities for essentially the same firm. These shell companies can pass money back and forth and offshore, lowering a business’ tax liability and making its income nearly impossible to track to a taxpayer.

The critical innovation is scale: While most pass-through businesses are legitimate small operations like law firms or restaurants, the ultra-wealthy have learned to legally disguise vast conglomerates as thousands of separate “small businesses,” exploiting a tax structure that was never intended for them. There is now more business income in pass-through businesses than in traditional C-corporations. Indeed, just partnerships, the most secretive and flexible type of pass-through business, now typically account for more business income than all C-corporations.

For this reason, any serious agenda to tax the rich must go beyond raising the corporate tax rate. Doing so without addressing pass-throughs could actually accelerate the rich’s shift toward cycling more of their income through shell companies. What’s needed is a Shell Company Tax, or a mechanism that reaches the sprawling pass-through empires hiding trillions of dollars across hundreds of thousands of entities. This will restore basic fairness and rationality to the business tax system.

The Amazing, Disappearing Corporate Tax

The corporate income tax is vanishing. In the 1960s, the United States collected 20 percent of federal tax revenues from corporations. By the 1980s, that share had fallen to 10 percent. The CBO now projects that going forward, only 7 percent of federal tax revenues will come from the corporate income tax.

What happened? The first part of the story may be familiar: The top corporate tax rate was cut from 52 percent in 1960, to 35 percent in the 1990s, to just 21 percent after the 2017 Tax Cuts and Jobs Act. Business deductions have also been expanded, most significantly for investments in equipment and manufacturing structures.

The second part of the equation is less well known: Corporate income moved. After 1980s tax reforms loosened rules around pass-through businesses—allowing limited liability companies (LLCs) to claim partnership tax treatment—the wealthy shifted aggressively from entities that pay corporate tax into tax-free businesses. To understand this, it is important to note that businesses can organize under several legal forms, and each is taxed differently:

- C-Corporations: Often publicly traded and recognizable businesses. They pay taxes under the corporate tax system and distribute dividends to shareholders, which are also taxed.

- Sole proprietorships: Pass-through businesses typically including “mom-and-pop” businesses and independent contractors. Owners pay taxes directly on their personal returns.

- Partnerships, S-corporations, and other pass-throughs (also called LLCs, LPs, and similar structures): Different types of pass-through businesses which do not usually pay federal taxes. Instead, income flows through to the partners with extraordinary flexibility, and there can be many layers of partners before income reaches an entity that is directly taxable.

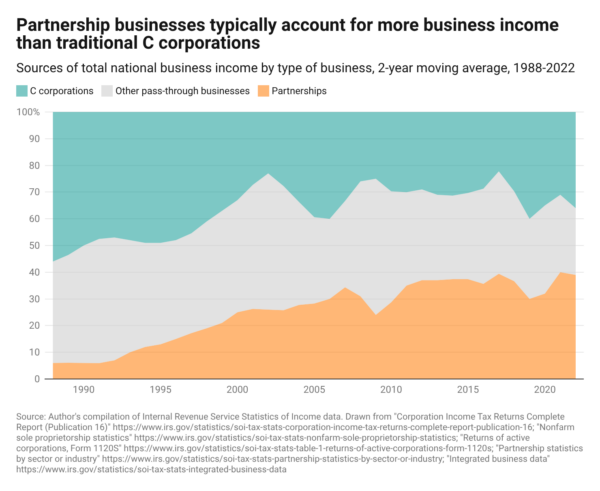

The different forms ultimately lead to different tax rates. One study put pass-through businesses’ average effective tax rate at 23.7 percent versus 29.3 percent for corporate income. Before most businesses received a tax rate cut in 2017, another study found that partnerships, the largest type of pass-through business, paid half the tax rate corporations paid. Low taxes are a primary reason why the rich have been moving their businesses out of the corporate sector and into pass-throughs (see figure).

“Partnerships” Now Make up More of Total Business Income Than Traditional Corporations

The shift is now decisive. Since the mid-1990s, the majority of U.S. business income has been earned by pass-through businesses instead of corporations. Since 2015, C-corporations have accounted for only 33 percent of reported business income, while partnerships alone account for 36 percent.

Partnerships are often everyday businesses like manufacturers, dentistry practices, and car dealerships. However, the IRS reports that most partnerships, including two-thirds of partnerships’ profits, come from just two sectors: “finance and insurance” and real estate.

“Finance and insurance” partnerships include huge private equity firms like Bain Capital or Sequoia. Private equity firms commonly funnel their capital gains and interest income overseas to “blocker corporations” and tax haven countries, which can allow these returns to escape U.S. tax entirely. One-sixth of partnership income goes overseas, mostly to tax havens.

Real estate firms are the next largest user of partnerships and other pass-through businesses. Famously, the Trump Organization is set up as hundreds of different entities. In illegally leaked tax returns, we saw that the President and his wife used a dizzying array of different business entities (foreign and domestic), “a curious pattern” of deductions, and other tax maneuvers en route to paying no taxes in 10 of 15 years, and only “$750 in federal income taxes the year he won the Presidency.” Since his businesses are generally pass-through businesses, that means the businesses that the President owns also paid little or no federal taxes those years, even if some of them were profitable.

If you care about inequality, low taxes on growing pass-through business income are a problem. Corporation income is very unequal—45 percent of it goes to the top 1 percent. However, pass-through business income is even more unequal—69 percent of it goes to the top 1 percent! In 2022, according to the CBO, the top 1 percent earned about a quarter of their income from pass-through businesses.

As of 2019, there were 20,000 “large partnerships” (those with $100 million or more in assets and 100 or more total partners) that collectively owned $16 trillion in assets. There were fewer than 17,000 similarly sized C-corporations. What’s more, these large partnerships together owned assets equal to the value of all the homes and real estate belonging to 90 percent of Americans in 2019.

If the goal is to have a fair taxation system where the wealthy pay their fair share, taxes need to follow the money, which means going after these private, pass-through businesses. The 1000 percent growth in pass-through business income among the top 1 percent shows that this is increasingly how the rich make their money. Distressingly, even apart from their already-low tax rates, pass-through businesses have become one of the best ways to avoid taxes entirely.

Playing Shell Games With the IRS

What if wealthy people could build entities that were functionally impossible for the IRS to audit? Turns out, they already have.

In October 2023, the IRS sent 483 “soft letters” to high-worth partnership businesses, flagging discrepancies in their tax filings. Of those, 163 went unanswered, and 182 responses were rejected for insufficient documentation. What happened next might surprise and depress you. The IRS pursued zero cases, including against the partnerships that ignored the letter entirely, citing lack of resources. Despite the apparent errors, each of those businesses was let off the hook.

Sadly, it may not have made a difference even if the IRS had pursued these companies. From 2010 to 2018, the IRS audited only 675 “large” partnerships (those with at least $100 million in assets and at least 100 partners)—an audit rate of less than 1 percent. And in the end the IRS collected no revenue on net from those partnership audits.

Over the same timeframe, the IRS audited over 24,000 similarly sized corporations, an audit rate of over 10 percent. In contrast to the above, when auditing these corporations, the IRS collected $4.5 million on average, netting over $100 billion in unpaid taxes in those years.

Are owners of large partnerships just more honest than large corporations on their taxes? Hardly. The word “partnership” evokes two friends running a business together, and many are exactly that. But when Congress created the modern partnership structure in the 1980s, it imposed no limits on assets, revenue, number of partners, or who—or what—could constitute a partner. The result is that many partnerships today are larger and more complex than any corporation you could name.

In an episode of the hit 2000s-era NBC sitcom 30 Rock, the character Jack Donaghy explained the complex corporate structure behind NBC. On Donaghy’s chart, General Electric—which owned NBC at the time—is depicted as consisting of dozens of shell companies. Here, the gag was that NBC was ultimately owned by the fictional “Sheinhardt Wig Company” and through the subsidiaries “pokerfastlane.com” and “KitchenAll.” Donaghy’s multilayered mess of an organizational chart is an all-too-real depiction of the labyrinthine structures the wealthy use to shield their wealth—and even then, it is too simple.

The key to partnerships’ ability to outfox the IRS is that partnerships now regularly consist of not dozens, but thousands of shell companies. Corporations sometimes have many subsidiary companies, but there are practical and tax limits to how far they can go down this road. In contrast, partnerships regularly own other partnerships that own a hundred other partnerships that each own other partnerships, that then own the original partnership—creating a Russian nesting doll of entities that allow people to hide billions in revenue and assets.

When the IRS comes to audit a large partnership for a missing tax payment, suspicious deduction, or other discrepancy, the partnership’s accountants need only point the IRS agent in another direction and wait for the statute of limitations to run out. “Oh, that revenue? Well, 3 percent of it came from this other partnership, 1 percent came from this partnership, and 4 percent went to a Cayman Islands fund…. Why don’t you go check with all one hundred of them and get back to us?”

This kind of run-around can take a full team of IRS agents years to track down, if it’s even possible at all. From 2010-2018 it took 2.99 years on average after filing a return for the IRS to finish an audit of a large partnership. The statute of limitations is three years, meaning almost all audits take the full amount of time allowed by law. “The IRS runs out of time” is cited by the Government Accountability Office (GAO) as the main reason audits of complex partnerships fail to turn up any revenue.

Unfortunately, the audit rate for partnerships with assets of $10 million or more has fallen from 2.5 percent in 2014 to 0.1 percent in 2023. The IRS knows this is a problem, telling the GAO that “tax practitioners may believe there is less enforcement in the partnership area, which has potentially encouraged the use of partnerships as vehicles for tax noncompliance.” In the 2022 Inflation Reduction Act (IRA), Congress boosted the IRS budget by $80 billion, which the agency said it would use to address tax compliance for “complex partnership structures, large corporations, and high-income individuals.” However, the current Congress and the Trump Administration have continually cut IRS audit staff and passed laws essentially rescinding all remaining IRA funds allocated to the IRS. The Trump Administration Fiscal Year 2027 IRS proposal states that they plan to continue reducing partnership audits, relative to 2021-2023.

Let’s recap. Pass-through businesses, especially of the “partnership” variety, are:

- The fastest growing type of income for the top 1 percent;

- Sending more than two-thirds of their income to the top 1 percent;

- Sending one in six dollars overseas;

- Growing increasingly complex;

- Facing lower tax rates than corporations;

- Representing more business income than corporations;

- And are almost never audited, let alone effectively.

So, what can be done about this? The answer is straightforward.

How to Untangle This Mess: Tax Shell Companies

The principle is simple: If a business makes money, someone immediately adjacent needs to be taxed on it. Individuals are taxed on their income. Corporations are taxed on their profits. Sole proprietorships pass income directly to their owners’ returns. There is no good reason for a class of businesses to earn money without paying taxes itself, or passing income directly to a real, taxable entity. A Shell Company Tax would close that loophole.

A Shell Company Tax could be straightforward. A business can remain tax-free if its profits pass directly to tax-paying owners or a genuine nonprofit like a charity or pension plan—the way pass-throughs are supposed to work. But if an untaxed business is “owned” by other untaxed businesses, it is a shell company, and it must pay a 1 percent tax on the amounts of income, deductions, and assets passed to another untaxed business entity. If a non-taxable partnership wants to have shell companies, it can have them—but not tax-free.

This tax would scale with complexity. The majority of partnerships are owned by individuals and remain untaxed. A law firm that is owned by its four partners could pass money tax-free to them, as it does now. But, private equity firm with one shell company layer incurs a 1 percent tax every time money passes from one untaxed business to another. Income, deductions, and assets that pass between two layers of shell companies incurs a 2 percent tax, and so on. For example, in 2019, the GAO reported that at least 6,000 partnerships had 20 or more tiers of shell companies. Under this Shell Company Tax, that money would face taxes of up to 20 percent on between-entity transfers. The incentive to simplify would be powerful.

How much money could this tax raise? Columbia University economist Michael Love estimates that in 2022, at least $4.4 trillion was passed in aggregate from one partnership to another, to overseas, or to another business. A 1 percent tax would have raised $44 billion that year. Over a decade, it would raise nearly $650 billion, if partnership income continues to grow at 9 percent per year (as it has since 1999).

If wealthy owners chose to dismantle their shell company structures instead of paying the tax, that would be an equally good outcome. Simple partnerships take much less time for the IRS to audit and return less in corrective payments (which means they are more likely to have filed correctly in the first place). A simpler partnership system with fewer shell companies is one where we can have more faith that taxes are being paid fully and audited accurately. If the IRS was able to recover missed taxes from partnership audits at the same rate it does from corporate audits—adjusted for business income growth from 2010-2018 to now—taxpayers would recover an additional $375 billion over the next decade.

Partnerships are meant to give a few small businesspeople a flexible way to pool assets and share ownership of a business. They have been abused by rich and powerful tycoons to lower their tax bills and shovel money overseas tax-free. Complex pass-through businesses are fueling rising inequality by allowing the rich to lower their tax rates and hide their business income from the IRS. Partnerships now regularly have more income than C-corporations. A Shell Company Tax would not eliminate pass-throughs; instead, it would bring an exploding sector back into balance by ensuring the most egregious abuses come with a price tag.

Source link democracyjournal.org

The 2016 Panama Papers investigation revealed how global elites, including associates of leaders and drug dealers, concealed wealth via shell companies and offshore tax havens, fueling inequality. Though fewer Americans were implicated, they similarly exploit domestic pass-through businesses, benefitting from lower taxes and minimal IRS scrutiny. Pass-through income for the top 1% has surged, significantly contributing to income inequality. Despite accounting for more business income than C-corporations, pass-through businesses often evade audits. Implementing a Shell Company Tax could address these loopholes, ensuring fair taxation and potentially generating significant revenue while discouraging complex and secretive business structures.